Escape the Payday Loan Trap and Rebuild Credit in Canada

Step-by-step guide for Canadians to break the payday loan cycle, handle collections, and rebuild credit. Provincial laws, recovery plan, and free tools.

Product Manager in Fintech · Montreal, Canada

Ready to start recovering? Our free quiz creates a personalized plan for your exact situation.

Take the Free Quiz →How Payday Loans Trap Canadians in a Debt Cycle

More than one million payday loans are issued in Canada every year. The borrowers are not reckless spenders. They are nurses, retail workers, gig drivers, and single parents who needed a few hundred dollars to cover an emergency and found that the fastest option was a storefront or online payday lender. The problem is not the first loan. The problem is the second, the third, and the tenth.

A payday loan in Canada is a short-term loan of $1,500 or less, typically due on your next payday. The dollar amounts sound small. The cost does not. At $15 per $100 borrowed, a $500 payday loan costs $75 in fees for a two-week term. Annualized, that translates to roughly 391 percent APR. By comparison, even a high-interest credit card charges 19.99 to 25.99 percent annually.

Here is how the cycle works in practice:

- The emergency. You borrow $500 because your car needs a repair and you do not have savings.

- The repayment shock. Two weeks later, $575 is withdrawn from your bank account. But your paycheque was only $1,400, and your rent, groceries, phone, and transit cost $1,350. You now have a $525 gap.

- The second loan. You borrow again, sometimes from a different lender, to cover the gap the first loan created.

- The spiral. Each cycle adds another $75 in fees. After three rollovers, you have paid $225 in fees on the original $500 and still owe the principal in full.

- The default. Eventually, you cannot keep up. The lender attempts to withdraw from your account, it bounces, your bank charges NSF fees of $45 to $48 each, and the payday lender sells the debt to a collection agency.

The Financial Consumer Agency of Canada (FCAC) has found that nearly half of payday loan borrowers take out more than one loan per year, and about a quarter take out seven or more. This is not a personal failing. It is the business model working exactly as designed.

The Financial Consumer Agency of Canada (FCAC) has found that nearly half of payday loan borrowers take out more than one loan per year, and about a quarter take out seven or more. This is not a personal failing. It is the business model working exactly as designed.

Not sure where you stand? Take our free credit score quiz to see what scenario matches your situation and get a personalized recovery roadmap.

What I See at Work Every Week

At the financial company where I work in Montreal, I see the payday loan cycle up close. Colleagues regularly help clients who owe $500 on a payday loan and are paying $50 per month just in interest. These people are not irresponsible — many of them had decent credit before a job loss, a divorce, or a medical emergency. One missed mortgage payment led to a credit score drop, which led to declined credit card applications, which left a payday lender as the only option. When I moved to Canada from Kyrgyzstan in 2022, I was surprised to learn that roughly 30 to 40 percent of Canadians carry credit scores below 600. In a country this wealthy, the number of people trapped in high-interest borrowing is staggering.

Provincial Payday Lending Laws Across Canada

Payday lending is regulated at the provincial level in Canada, which means your rights and protections depend on where you live. Knowing your provincial rules is critical because if a lender has overcharged you, you may be owed a refund and can file a complaint.

Ontario

Ontario’s Payday Loans Act, 2008 is one of the most detailed payday lending frameworks in the country. Key provisions include:

- Maximum cost of borrowing: $15 per $100 borrowed.

- Cooling-off period: You have two full business days after receiving the loan to cancel without penalty and return the principal.

- Licensing requirement: All payday lenders must be licensed by the Ontario Ministry of Public and Business Service Delivery. Unlicensed lenders are operating illegally.

- No rollovers: A payday lender in Ontario cannot issue you a new loan to pay off an existing one. This anti-rollover provision is designed to prevent the exact debt cycle described above.

- Disclosure: The lender must provide a written agreement showing the total cost of borrowing in dollars and as an APR before you sign anything.

If you believe an Ontario payday lender has violated any of these rules, file a complaint with the Ministry at 1-800-889-9768.

British Columbia

- Maximum cost of borrowing: $15 per $100 borrowed.

- Cooling-off period: None mandated by statute, but the loan agreement must include clear cancellation terms.

- Repeat borrowing restrictions: BC’s Business Practices and Consumer Protection Authority (BPCPA) monitors lenders for patterns of repeat lending to the same borrower.

- Complaints: File with Consumer Protection BC at 1-888-564-9963.

Alberta

- Maximum cost of borrowing: $15 per $100 borrowed.

- Cooling-off period: Two business days to cancel and return the principal.

- Collection restrictions: Alberta has specific rules prohibiting payday lenders from using continuous payment authority (repeatedly attempting to withdraw from your account after a failed attempt).

- Licensing: Consumer Protection Alberta licenses and audits payday lenders.

- Complaints: File at 1-877-427-4088.

Other Provinces

- Manitoba: $17 per $100 (higher than most other provinces).

- Saskatchewan: $17 per $100.

- New Brunswick: $15 per $100.

- Nova Scotia: $19 per $100 (the highest rate in Canada).

- Prince Edward Island: $15 per $100.

Quebec effectively banned payday lending by capping the total cost of credit at 35 percent annually under the Consumer Protection Act, making the payday loan business model unviable in the province.

Important: If any lender, whether online or in a storefront, has charged you more than your province allows, you can file a complaint with your provincial consumer protection office and potentially recover the overcharge.

The Credit Damage Payday Loans Cause

Payday loans damage your credit through several mechanisms at once, which is why the score impact can be severe and long-lasting.

Collections accounts are the most damaging. When you default on a payday loan, the lender typically sells the debt to a third-party collection agency within 90 days. That collection agency then reports the account to Equifax and TransUnion. A single collections entry can drop your score by 80 to 150 points, and it remains on your report for six years from the date of last activity in most provinces (seven years in some).

Multiple hard inquiries compound the problem. Each payday loan application generates a hard inquiry on your credit report. If you applied with five different lenders in a single month, that is five inquiries, signalling severe financial distress to anyone reviewing your file. Each inquiry stays on your report for three years.

NSF records and bank account closures create a secondary layer of damage. Repeated NSF charges can cause your bank to close your account. While this does not directly appear on your Equifax or TransUnion report, it can be flagged in internal bank databases, making it difficult to open a new account elsewhere.

Simultaneous defaults are common because many borrowers have multiple payday loans at once. Each default creates its own collections entry, so it is not unusual to see three, four, or five separate payday loan collections on a single credit report.

Use our free credit score calculator to estimate where your score might be now and how much it could improve over the next 12 months with consistent rebuilding.

Breaking Free: How to Stop the Payday Loan Cycle

Step 1: Stop Taking New Payday Loans

No rebuilding strategy works if you are still borrowing at 391 percent interest. This is the hardest step because the gap the loans were filling does not disappear. Here are concrete alternatives:

- Credit union emergency loans. Many Canadian credit unions, including Vancity, Desjardins, and local community credit unions, offer small-dollar loans of $500 to $1,500 at interest rates between 19 and 26 percent. This is still expensive credit, but it is a fraction of the payday loan cost.

- Dial 211. Calling 2-1-1 connects you with local community services anywhere in Canada. This includes emergency food banks, rent banks that provide interest-free loans for rent and utility arrears, clothing programs, and referrals to financial assistance.

- Employer payroll advances. Some employers will advance your next paycheque at no cost. Ask your HR department.

- Provincial emergency assistance. Ontario Works, BC Employment and Assistance, Alberta Works, and equivalent programs in every province provide emergency financial help. The application processes vary, but this money does not need to be repaid.

- Community micro-loans. Some non-profits, such as Momentum in Calgary and the Canadian Alternative Financial Services Association member organizations, offer micro-loans as direct payday loan alternatives.

Step 2: Know Your Rights with Existing Loans

If you currently have outstanding payday loans:

- You are within the cooling-off period (two business days in Ontario and Alberta) and want to cancel, return the principal amount and the loan is void.

- If you are outside the cooling-off period but the lender is charging more than the provincial maximum, gather your loan documents and file a formal complaint with your provincial consumer protection office.

- If an online lender operating from outside Canada is charging you rates above provincial limits, report them to your provincial regulator. They may not be licensed to lend in your province at all.

Step 3: Talk to a Non-Profit Credit Counsellor

Credit Counselling Canada (creditcounsellingcanada.ca) is the national association for accredited non-profit credit counselling agencies. A counsellor can review your full financial picture for free and help you decide between the following options:

- Informal repayment plan. The counsellor contacts your payday lenders directly and negotiates reduced or eliminated interest and a single monthly payment you can afford.

- Debt Management Plan (DMP). A formal program where you make one monthly payment to the credit counselling agency, which distributes it to your creditors. Interest is typically reduced to zero. A DMP is noted on your credit report as R7, which is less severe than the R9 rating from collections or bankruptcy.

- Consumer proposal. If your total debt exceeds what you can repay through a DMP, a consumer proposal filed through a Licensed Insolvency Trustee (LIT) allows you to settle your debts for a percentage of what you owe, typically 30 to 70 cents on the dollar, paid over up to five years. Learn more in our detailed guide on how consumer proposals affect your credit in Canada.

Dealing with Payday Loan Collections in Canada

If your payday loans have already gone to collections, you need a strategy. Acting without a plan can actually make things worse.

Know What Collectors Cannot Do

Collection agencies in Canada are regulated by provincial law. They cannot:

- Call you before 7 a.m. or after 9 p.m. in your time zone.

- Contact you on statutory holidays.

- Contact your employer for any reason other than confirming your employment or getting your address.

- Use threatening, abusive, or profane language.

- Misrepresent the amount you owe or claim you could be arrested.

- Continue contacting you by phone after you send a written request (letter or email) asking them to communicate only in writing.

- In Ontario, contact you more than three times in a seven-day period (Collection and Debt Settlement Services Act, 2017).

If a collector violates any of these rules, document the call (date, time, what was said, the agent’s name) and file a complaint with your provincial consumer affairs office.

Limitation Periods by Province

A limitation period is the window of time during which a creditor or collection agency can sue you for an unpaid debt. After this period expires, the debt is “statute-barred,” meaning it cannot be enforced through the courts. However, the debt can still appear on your credit report.

Key limitation periods for most consumer debts:

| Province | Limitation Period |

|---|---|

| Ontario | 2 years |

| British Columbia | 2 years |

| Alberta | 2 years |

| Manitoba | 6 years |

| Saskatchewan | 2 years |

| Quebec | 3 years |

| New Brunswick | 6 years |

| Nova Scotia | 6 years |

| PEI | 6 years |

| Newfoundland | 6 years |

Critical warning: In some provinces, making a payment or even acknowledging the debt in writing can restart the limitation period clock. Before you pay anything to a collection agency, understand your province’s rules or consult a credit counsellor.

Pay-for-Delete Negotiation

A pay-for-delete is an arrangement where a collection agency agrees to remove the collections entry from your credit report entirely in exchange for full payment of the debt. This is the best possible outcome when dealing with collections because it erases the negative mark rather than just changing the status to “paid.”

Here is how to approach it:

- Never acknowledge the debt on the phone. Ask the collector to send you written verification of the debt, including the original creditor name, account number, and amount.

- Verify the debt is accurate. Compare the collection notice to your records. If there are errors, dispute the entry directly with Equifax and TransUnion. You can use our free dispute letter template to draft your dispute.

- Make a written pay-for-delete offer. Send a letter offering to pay the full amount in exchange for complete removal of the collections entry from both Equifax and TransUnion. Use our free pay-for-delete letter template to get started.

- Get the agreement in writing. Do not pay until you have a signed letter from the collection agency confirming the pay-for-delete terms.

- Pay by money order or certified cheque. Do not give the collection agency access to your bank account via pre-authorized debit.

- Follow up. After paying, check your credit report in 30 to 60 days to confirm the entry has been removed. If it has not, contact the agency with a copy of the written agreement.

Not every collection agency will agree to a pay-for-delete, but many will, especially for smaller payday loan debts. The agency typically paid pennies on the dollar for your debt, so receiving full payment is profitable for them regardless.

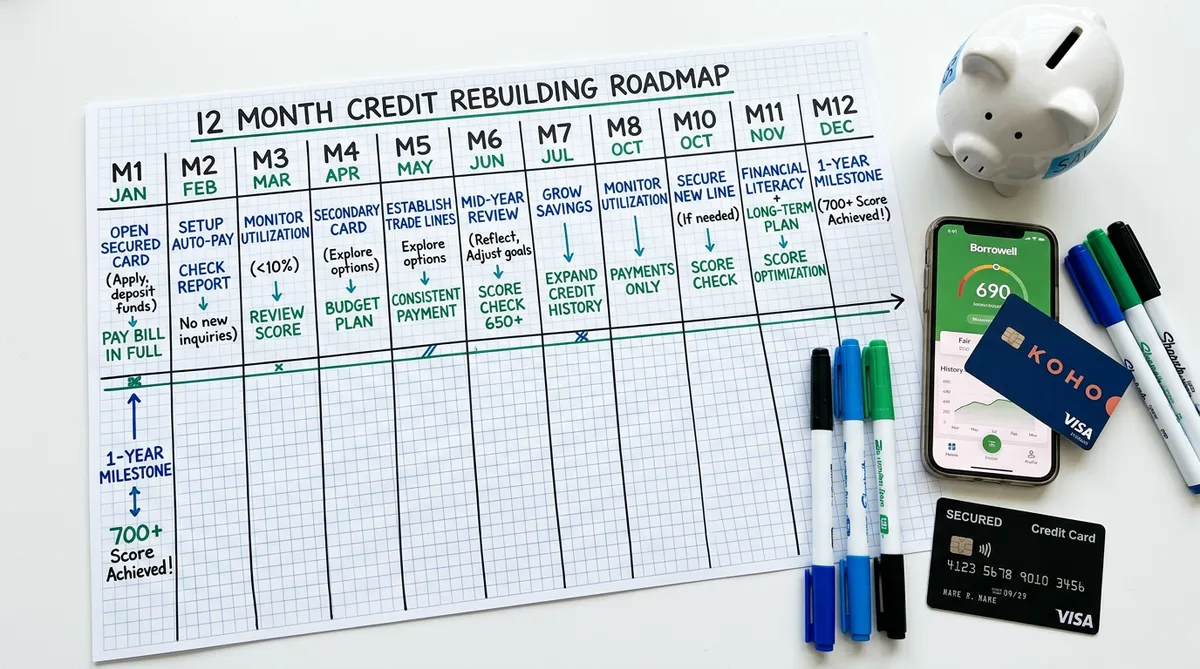

Month-by-Month Credit Rebuilding Plan

Once you have stopped the payday loan cycle and addressed your collections, it is time to rebuild. Here is a concrete 12-month plan.

Month 1: Assess and Monitor

- Sign up for Borrowell to get free weekly access to your Equifax credit score and full credit report. Review every item on your report.

- Dispute any errors you find. Incorrect balances, debts listed twice, and collections from lenders you never borrowed from are all common. See our step-by-step dispute guide.

- Open a free budgeting account with KOHO to separate your spending from your bill-payment account. KOHO uses a prepaid model, which means no overdraft fees and no risk of NSF charges.

Month 2: Establish a Basic Bank Account

If your bank account was closed due to NSF activity, you need a new one. Under federal regulations (the Access to Basic Banking Services Regulations), every Canadian has the right to open a personal bank account at any bank, even if you have been declined before. Bring two pieces of ID to any bank branch. If you are refused, file a complaint with the Financial Consumer Agency of Canada (FCAC).

Month 3: Apply for a Secured Credit Card

A secured credit card is the single most effective tool for rebuilding damaged credit. You provide a refundable security deposit, and the issuer gives you a credit card with a limit equal to (or close to) that deposit. Your payment activity is reported to Equifax and TransUnion monthly, building your history with every on-time payment.

The Capital One Secured Mastercard is widely available to Canadians with damaged credit and requires a deposit starting at $75. For a detailed comparison of all your options, read our guide on the best secured credit cards for bad credit in Canada in 2026.

Rules for using your secured card:

- Keep utilization under 30 percent of your limit. If your limit is $300, never have more than $90 on the card at any time.

- Pay the full statement balance by the due date every month. Set up an automatic payment from your bank account.

- Use the card for one or two small recurring expenses, such as a streaming subscription or a monthly transit pass.

- Never use the card for cash advances.

Months 4 to 6: Build Consistency

- Continue paying your secured card in full and on time every month. Payment history accounts for 35 percent of your credit score.

- If you have any remaining payday loan debts, continue your repayment plan through your credit counsellor or DMP.

- Track your score through Borrowell. You may start to see small improvements by month 5 or 6, typically 10 to 30 points.

- Build an emergency fund, even if it is only $25 per paycheque. This is your buffer against the next unexpected expense that might otherwise push you back toward a payday lender.

Months 7 to 9: Add a Second Credit Product

- Consider adding a credit-building product like the KOHO Credit Builder, which reports to Equifax for a small monthly fee. Having two active credit accounts reporting on time is better than one, because it shows lenders you can manage multiple obligations.

- If you have a cellphone plan, confirm with your provider that they report to the credit bureaus. Some do, and on-time payments help.

- Continue monitoring your report for errors and ensuring all payments are being reported correctly.

Months 10 to 12: Evaluate and Plan Ahead

- By month 10 to 12, consistent on-time payments should produce a noticeable score improvement, often 50 to 100 points above where you started.

- Do not apply for new credit products yet. Each application creates a hard inquiry. Wait until your score has recovered to at least 600 before considering an unsecured credit card.

- Review your full credit report again. Confirm that any pay-for-delete agreements have been honoured and that disputed errors have been corrected.

- Revisit our credit score calculator to see your updated estimate and plan your next steps.

Where are you in your recovery? Take the credit recovery quiz to get a personalized action plan based on your current situation.

Consumer Proposals: When Payday Debt Is Too Large to Manage Alone

If your payday loan debt has ballooned into thousands of dollars, possibly combined with credit card debt, medical bills, or other obligations, a consumer proposal may be your best path forward. A consumer proposal is a legally binding agreement between you and your creditors, filed through a Licensed Insolvency Trustee (LIT), where you repay a portion of your total debt over a period of up to five years.

Key advantages over bankruptcy:

- You keep your assets (home, car, RRSP contributions made more than 12 months ago).

- Your credit report shows R7 instead of R9, which is less damaging.

- The notation is removed from your credit report three years after you complete the proposal (or six years from the filing date, whichever comes first).

- Creditor collection calls and wage garnishments stop immediately upon filing.

A consumer proposal typically costs between $1,500 and $15,000 in total, depending on the amount of debt and the settlement percentage your creditors accept. The LIT’s fees are included in your monthly payments, so there is no additional out-of-pocket cost.

Read our complete guide to consumer proposals and credit recovery in Canada for detailed timelines, costs, and rebuilding strategies.

Free Resources for Canadians in Payday Loan Debt

You do not have to navigate this alone. These organizations exist specifically to help:

- Credit Counselling Canada (creditcounsellingcanada.ca): The national association for accredited non-profit credit counselling agencies. Free consultations, Debt Management Plans, and financial education.

- 211 Canada (211.ca or dial 2-1-1): Available 24/7 in most areas. Connects you to local emergency financial assistance, food banks, rent banks, utility help, clothing programs, and mental health support.

- Financial Consumer Agency of Canada (fcac-acfc.gc.ca): Complaint handling for federally regulated financial institutions, educational resources about your borrowing rights, and budgeting tools.

- Your provincial consumer protection office: File complaints about payday lenders and learn about provincial regulations.

- Provincial legal aid programs: If a collection agency is harassing you or a payday lender has violated the law, you may qualify for free legal help through legal aid (Legal Aid Ontario, Legal Services Society in BC, Legal Aid Alberta, etc.).

- Our free tools: Use our dispute letter generator and pay-for-delete letter template to handle collections. Try the debt repayment calculator to see how quickly you can become debt-free.

FAQ

Can payday loans affect my credit score even if I repay on time?

Generally, payday loans that are repaid on time and in full do not appear on your Equifax or TransUnion credit report, because most payday lenders do not report to the credit bureaus. The damage occurs when you default and the debt goes to a collection agency, which does report. However, the hard inquiries from applying for payday loans do appear on your report and can lower your score by a few points each. Multiple inquiries in a short period signal financial distress to lenders reviewing your file.

How long do payday loan collections stay on my credit report in Canada?

A collections account from a payday loan stays on your credit report for six years from the date of last activity in most provinces. The “date of last activity” is typically the date of your last payment or the date the account was sent to collections, whichever is later. In some provinces, making a payment on an old collections account can reset this clock, so consult a credit counsellor before paying anything. After the six-year period, the entry is automatically removed by the credit bureau.

Should I pay off old payday loan collections or wait for them to fall off?

This depends on several factors: how old the debt is, whether the limitation period has expired, and whether you need to improve your credit soon (for example, to qualify for a mortgage or rental application). If the debt is close to falling off your report (within a year of the six-year mark), paying it could reset the reporting clock. If the debt is relatively new, negotiating a pay-for-delete agreement is usually the best strategy because it removes the entry entirely. For debts past the limitation period, you cannot be sued, but the entry still affects your score until the six-year reporting period ends. Use our pay-for-delete letter template to start the negotiation.

Are online payday lenders legal in Canada?

Online payday lenders must be licensed in the province where the borrower lives, not just where the lender is based. If an online lender is charging you more than your provincial maximum or is not licensed in your province, they are operating illegally. Check with your provincial consumer protection office to verify a lender’s licence. Unlicensed lenders have no legal standing to collect the debt, and you can report them. Be especially cautious of lenders based outside Canada that advertise to Canadian borrowers, as they often charge rates far above provincial caps and use aggressive, unlawful collection tactics.

Can I file for bankruptcy just for payday loan debt?

You can, but bankruptcy is usually an extreme option for payday loan debt alone. A consumer proposal is typically a better choice because the credit impact is less severe (R7 vs. R9) and you keep your assets. Bankruptcy stays on your credit report for six years after discharge for a first-time bankruptcy and fourteen years for a second. A consumer proposal is removed three years after completion. If your total debts, including payday loans, credit cards, and other obligations, exceed $250,000 (excluding your mortgage), you would need to file a Division I proposal instead of a consumer proposal. Talk to a Licensed Insolvency Trustee for a free assessment of your options.

This article contains affiliate links to financial products that we have independently reviewed and believe may benefit readers in credit recovery situations. If you sign up through these links, we may earn a commission at no extra cost to you. This does not influence our recommendations. All information is intended for educational purposes and does not constitute financial, legal, or tax advice. Consult a qualified professional for advice specific to your situation. Payday lending regulations and limitation periods are current as of March 2026 and may change. Always verify with your provincial consumer protection office.

Get Your Personalized Recovery Plan

Answer 6 quick questions and get a step-by-step plan tailored to your situation.

Take the Free Quiz

Product manager in fintech, immigrant to Canada, and founder of Credit Score Hero. I moved from Kyrgyzstan to Montreal in 2022 and built this site to help Canadians navigate the credit system with free tools and honest, Canada-specific advice.

Related Recovery Guides

After Bankruptcy

Month-by-month recovery plan for Canada

After Divorce

How to recover your credit after separation

Student Debt Recovery

Guide for Canadians with student debt problems

Best Secured Cards 2026

Compare secured credit cards for rebuilding in Canada

Renting with Bad Credit (Ontario)

Your rights as a renter under the Human Rights Code