Rebuild Credit After Bankruptcy in Canada: Monthly Plan

A detailed timeline for rebuilding your credit after bankruptcy or consumer proposal in Canada. Month-by-month steps with recommended tools.

Product Manager in Fintech · Montreal, Canada

Ready to start recovering? Our free quiz creates a personalized plan for your exact situation.

Take the Free Quiz →Understanding Bankruptcy’s Impact on Your Credit

Filing for bankruptcy in Canada is one of the most difficult financial decisions you can make, but it is also a legal fresh start. A first-time bankruptcy stays on your credit report for six years after your discharge in most provinces (seven years in some). A consumer proposal remains for three years after completion or six years after filing, whichever comes first.

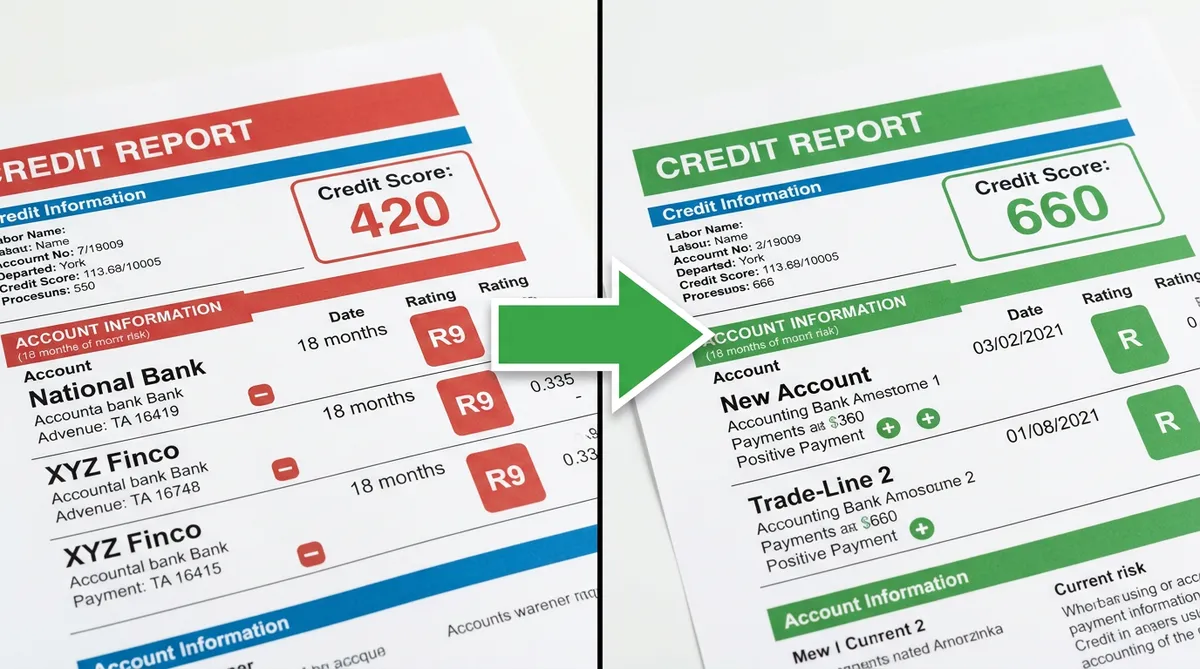

During this period your credit score can drop to the 300-450 range. Equifax assigns an R9 rating (the lowest possible) to accounts included in bankruptcy, and an R7 rating for consumer proposals. Both make it nearly impossible to access traditional credit products right away.

The good news: you do not have to wait six years to start rebuilding. Many Canadians reach a credit score above 650 within 18 to 24 months of their discharge by following a consistent plan.

Why I Know This Works

I work as a product manager at a financial company in Montreal, and I see what happens to people after bankruptcy every day. The most important thing I have learned: the people who start rebuilding immediately after discharge consistently end up in a better place than those who wait. I moved to Canada from Kyrgyzstan in 2022 and built my own credit from scratch — from zero history to 820 in about three years. The principles are the same whether you are starting from no credit or recovering from bankruptcy: secured card, on-time payments, low utilization, patience. The timeline is longer after bankruptcy, but the strategy works.

I was surprised to learn that roughly 30 to 40 percent of Canadians carry scores below 600. Many of them got there through a bankruptcy. The worst part is what comes after: traditional banks will not work with them, so they end up at payday lenders paying 400% APR. That cycle is avoidable if you follow the plan below. For a detailed look at escaping payday lender debt, see our guide on the payday loan trap and rebuilding credit.

Here is exactly what to do each month.

Month 1-2: Lay the Foundation

Get Your Free Credit Report

Before you do anything else, pull your credit reports from both Equifax Canada and TransUnion Canada. You are entitled to a free copy of each report once per year by mail, or you can use a free monitoring service. Borrowell provides free weekly Equifax score updates and is one of the best ways to track your progress over time.

Review every line of your report carefully. Verify that all debts included in your bankruptcy or proposal show a zero balance. If any discharged debts still appear as active or owing, dispute them directly with the credit bureau. Errors are common and can drag your score down unnecessarily.

Build a Post-Bankruptcy Budget

Your Licensed Insolvency Trustee (LIT) likely helped you create a basic budget, but now is the time to refine it. Focus on three goals:

- Build an emergency fund. Even $500 in savings can prevent you from falling back into debt when unexpected expenses arise.

- Pay every bill on time. Utilities, phone bills, and rent are not always reported to the bureaus, but missed payments on any obligation can end up in collections and damage your score further.

- Avoid any new debt you cannot repay immediately. This phase is about stability, not growth.

Open a Basic Banking Account

If you do not already have a chequing account, open one at a major bank or credit union. Under the federal Access to Basic Banking Services regulations, no Canadian bank can refuse you a basic account due to bankruptcy. Consider a digital banking option like KOHO, which offers a prepaid Mastercard that helps you manage spending without the risk of overdraft.

Month 3-4: Start Building New Credit

Apply for a Secured Credit Card

A secured credit card is the single most important tool for rebuilding credit after bankruptcy. You provide a refundable security deposit (typically $200 to $500), and the card issuer gives you a credit limit equal to that deposit. The Capital One Secured Mastercard is one of the most accessible options in Canada, requiring a minimum deposit of $75. For a full comparison of your options, check our guide on the best secured credit cards for bad credit in Canada.

Use the card for one or two small recurring purchases each month, such as a streaming subscription or your phone bill. Keep your utilization below 30 percent of the limit and pay the full statement balance by the due date every single month. This builds a pattern of on-time payments that the credit bureaus reward.

Report Your Rent Payments

Rent is likely your largest monthly expense, so why not get credit for paying it? Services like Chexy report your rent payments directly to the credit bureaus. Since on-time payment history makes up roughly 35 percent of your credit score, adding rent reporting can accelerate your recovery significantly.

Month 5-8: Build Consistently

Maintain Perfect Payment Habits

Consistency is everything during this phase. Continue using your secured card for small purchases and paying in full every month. Do not apply for additional credit products yet. Every hard inquiry costs you a few points, and too many inquiries in a short period signals desperation to lenders.

Monitor Your Progress

Check your score monthly through Borrowell. You should start seeing upward movement by month four or five. Do not panic if progress feels slow. The credit scoring algorithm rewards time and consistency above all else.

Check your score monthly through Borrowell. You should start seeing upward movement by month four or five. Do not panic if progress feels slow. The credit scoring algorithm rewards time and consistency above all else.

Increase Your Secured Deposit

If your card issuer allows it, increase your security deposit to raise your credit limit. A higher limit with the same low spending gives you a lower utilization ratio, which helps your score. Some issuers review your account after six months and may offer an automatic limit increase.

Month 9-12: Level Up Your Credit Profile

Apply for a Second Credit Product

Once you have nine to twelve months of perfect payment history on your secured card, consider adding a second credit product. This could be:

- A credit-builder loan from a credit union. These small loans hold the funds in a locked savings account while you make monthly payments.

- A second secured card from a different issuer to build relationships with more than one lender.

- A small RRSP loan from your bank, which serves double duty by building credit and retirement savings.

Having two active credit accounts reporting on-time payments is better than one. Credit mix counts for about 10 percent of your score.

Request Your Secured Deposit Back

After 12 months of perfect payments, contact your card issuer and ask if you qualify for an upgrade to an unsecured card. Many issuers, including Capital One, will graduate your secured card to a regular card and refund your deposit. This is a major milestone in your recovery.

Set Goals for Year Two

By the 12-month mark, many people following this plan have a credit score in the 600-650 range. In year two, your goals shift to:

- Qualifying for an unsecured credit card with a modest rewards program.

- Building toward a score of 680 or higher, which opens the door to competitive interest rates on car loans and eventually mortgages.

- Continuing to keep utilization low and payments perfect.

Frequently Asked Questions

Can I get a mortgage after bankruptcy in Canada?

Yes, but timing matters. Most traditional lenders (A-lenders) require that your bankruptcy be discharged for at least two years and that you have re-established credit with a score above 680. Some B-lenders will consider applications sooner at higher interest rates. CMHC-insured mortgages typically require the bankruptcy to be fully removed from your credit report.

Is a consumer proposal better than bankruptcy for my credit?

A consumer proposal carries an R7 rating rather than R9, and it may fall off your report sooner (three years after completion versus six years after discharge for bankruptcy). However, both require the same rebuilding strategy. The choice between them depends on your total debt, income, and assets. Read our detailed guide on consumer proposals and credit impact in Canada for the full comparison. Consult a Licensed Insolvency Trustee for personalized advice.

How long until my credit score is normal again?

Most people who follow a consistent rebuilding plan see their score reach the 650-700 range within 18 to 24 months of their discharge. Reaching 750 or higher typically takes three to four years. The key factors are on-time payments, low utilization, and time.

Should I use a credit repair company?

Be cautious. In Canada, no company can legally remove accurate information from your credit report. Legitimate credit counselling agencies such as those accredited by Credit Counselling Canada can help you build a plan, but avoid any company that promises to erase your bankruptcy from your report.

Ready to start your recovery? Take our 90-second recovery quiz for a personalized rebuilding plan based on your current score and situation. If you spot errors on your credit report that should not be there, use our free dispute letter template to challenge them with the bureaus. And use our credit score calculator to estimate how much those corrections could improve your score.

Get Your Personalized Recovery Plan

Answer 6 quick questions and get a step-by-step plan tailored to your situation.

Take the Free Quiz

Product manager in fintech, immigrant to Canada, and founder of Credit Score Hero. I moved from Kyrgyzstan to Montreal in 2022 and built this site to help Canadians navigate the credit system with free tools and honest, Canada-specific advice.

Related Recovery Guides

After Divorce

How to recover your credit after separation

Student Debt Recovery

Guide for Canadians with student debt problems

After Payday Loans

Rebuilding credit after the payday loan trap

Best Secured Cards 2026

Compare secured credit cards for rebuilding in Canada

Renting with Bad Credit (Ontario)

Your rights as a renter under the Human Rights Code