KOHO Credit Builder Review 2026: Worth It?

An honest review of KOHO Credit Builder for Canadians. How it works, pros and cons, cost breakdown, and comparison with Borrowell Credit Builder and Refresh Financial.

Product Manager in Fintech · Montreal, Canada

Ready to start recovering? Our free quiz creates a personalized plan for your exact situation.

Take the Free Quiz →What Is KOHO Credit Builder?

If you have been searching for a low-barrier way to build credit in Canada, you have probably come across KOHO. KOHO is a Canadian fintech company that offers a prepaid reloadable Mastercard, a spending account, and a suite of financial tools through its mobile app. The Credit Builder feature is an add-on that lets you build credit history without needing a traditional credit card or a large security deposit.

The core idea is straightforward. You subscribe to a KOHO plan that includes Credit Builder. Each month, KOHO sets aside a small amount from your account balance (as low as $10), holds it in a dedicated savings-like account, and reports that activity to Equifax Canada as an installment loan being repaid on time. You are essentially creating a verified track record of on-time payments that Equifax records on your credit file.

Unlike a secured credit card where you need to put down $200 or more upfront, KOHO Credit Builder works with money you already have in your account. There is no hard credit check to sign up, no minimum credit score requirement, and no risk of going into debt since you are only using your own funds.

How Much Does KOHO Credit Builder Cost?

KOHO offers several subscription tiers, and Credit Builder is included with all paid plans. Here is a breakdown of the monthly costs as of early 2026:

- Essential plan: $7 per month. This is the entry-level paid plan that includes Credit Builder. You also get 1% cash back on groceries and transportation, plus access to financial insights and spending categorization in the app.

- Extra plan: $9 per month. Everything in Essential, plus higher cash back rates (up to 2% on select categories), coverage for purchase protection, and additional perks like price drop protection.

- Everything plan: $15 per month. The premium tier includes all features, the highest cash back rates, and extras like cell phone insurance and identity theft protection.

If your only goal is credit building, the $7 Essential plan is all you need. Over a full year, that comes to $84. Over two years, which is roughly how long most people use a credit builder product, you are looking at $168 in total fees. That is not nothing, but it is significantly less than the opportunity cost of having poor credit when you need a car loan or a lease approval.

There is no annual fee beyond the monthly subscription, and KOHO does not charge you interest since the Credit Builder uses your own money rather than extending you a line of credit.

How Does KOHO Build Your Credit?

KOHO Credit Builder reports your payment activity to Equifax Canada each month. Here is what happens behind the scenes:

- You set your Credit Builder amount. When you activate the feature, you choose how much to set aside each month, starting at $10. This money comes from your KOHO balance.

- KOHO holds the funds. The amount is moved into a reserved portion of your account. Think of it like a forced micro-savings plan.

- KOHO reports to Equifax. Each month, KOHO reports an on-time installment payment to Equifax Canada. This appears on your Equifax credit report as a tradeline with consistent on-time payments.

- Your funds are returned. At the end of the Credit Builder cycle, your money is released back to your available balance. You never lose the principal.

The key credit-building mechanism is payment history, which accounts for approximately 35% of your credit score under Canadian scoring models. By generating a steady stream of on-time payment reports, KOHO Credit Builder helps you establish or strengthen the most important factor in your score.

It is worth noting that results vary. Some users report seeing a noticeable score improvement within three to four months, while others take six months or longer to see meaningful movement. Your starting point matters. If you have a completely empty credit file, adding even one tradeline can produce a faster initial jump than if you already have several accounts with mixed history.

Would I Use KOHO Credit Builder?

I do not use KOHO Credit Builder myself. By the time I learned about it, I already had a CIBC credit card and my Equifax score through Borrowell was climbing past 700. But if I could go back to July 2022 when I first arrived in Montreal from Kyrgyzstan with absolutely zero Canadian credit history, this is exactly the kind of product I would have started with. When I got my first credit card at CIBC, my score dropped from 750 to around 700 because of the hard inquiry and new account. With KOHO, there is no hard inquiry, no risk to your existing score, and you start building Equifax payment history from day one. For $7 a month, that trade-off would have been worth it during my first six months in Canada.

Pros of KOHO Credit Builder

No Hard Credit Check

Signing up for KOHO does not trigger a hard inquiry on your credit report. This is a significant advantage over traditional credit products. Hard inquiries temporarily lower your score by a few points and stay on your report for up to three years in Canada. If your credit is already fragile, avoiding unnecessary hard pulls matters.

Low Monthly Cost

At $7 per month on the Essential plan, KOHO is one of the most affordable credit-building tools available in Canada. A secured credit card may not have a monthly fee, but it requires a deposit of $75 to $500 or more that is locked up for months or years. If you cannot afford to tie up that much cash, KOHO offers a viable alternative.

It Doubles as a Spending Account

Unlike standalone credit builder products, KOHO is also a fully functional spending account. You get a prepaid Mastercard accepted everywhere Mastercard is taken, the ability to receive direct deposits (including payroll), Interac e-Transfer support, and free ATM withdrawals at certain networks. You can use it as your everyday bank account, which means you are not paying $7 per month for a single-purpose tool.

Cash Back on Purchases

Even the $7 Essential plan includes cash back on groceries and transportation. The Extra and Everything plans offer higher rates. Over the course of a year, these earnings can offset a portion of your subscription cost, making the effective price of credit building even lower.

No Risk of Debt

Because KOHO Credit Builder uses your own money, there is zero chance of accumulating debt or paying interest. This is particularly important for people who are rebuilding after a difficult financial period and cannot afford the temptation or risk of a revolving credit line.

Cons of KOHO Credit Builder

Only Reports to Equifax, Not TransUnion

This is the single biggest drawback. KOHO Credit Builder reports exclusively to Equifax Canada. It does not report to TransUnion Canada. In Canada, different lenders pull from different bureaus. If you apply for a mortgage and the lender checks TransUnion, your KOHO payment history will not appear on that report.

For comprehensive credit building, you ideally want tradelines reporting to both bureaus. If you pair KOHO with a Capital One Secured Mastercard, which reports to both Equifax and TransUnion, you cover both bases.

The Monthly Fee Adds Up

While $7 per month is affordable, it is not free. Over 12 months you spend $84, and over 24 months you spend $168. A secured credit card, by contrast, typically has no monthly fee. Your deposit is refundable, and the only real cost is ensuring you pay your balance on time. If you can afford the upfront deposit for a secured card, the total cost of ownership may be lower than KOHO over a two-year period.

No Secured Credit Card Line

KOHO Credit Builder does not give you an actual credit card. It does not contribute to your revolving credit utilization metrics, which make up roughly 30% of your credit score. A secured credit card creates a revolving tradeline that demonstrates your ability to manage a credit limit responsibly. KOHO creates an installment tradeline, which is valuable but serves a different purpose in the scoring model.

For the strongest possible credit profile, you want both installment and revolving tradelines. KOHO alone does not give you the full picture.

Limited Impact for Established Credit Files

If you already have three or four active tradelines and a score in the mid-600s, adding KOHO Credit Builder is unlikely to produce a dramatic improvement. The product delivers the most value for people with thin files (few or no tradelines) or those starting from scratch. If you already have some credit history and are looking to optimize, your efforts may be better spent on improving utilization ratios or addressing negative items on your report. Take our recovery quiz to find out which strategy fits your situation.

Who Is KOHO Credit Builder Best For?

KOHO Credit Builder is not for everyone, and that is fine. Here is who benefits the most:

Newcomers to Canada

If you recently arrived in Canada and have no Canadian credit history, KOHO is an excellent starting point. You can sign up without a credit check, start building a tradeline immediately, and use the prepaid card for everyday spending while you get established. Many newcomers pair KOHO with a secured card to build two tradelines simultaneously.

Low-Income Canadians

If you cannot afford the $200 to $500 deposit required for most secured credit cards, KOHO lets you start building credit with as little as $10 per month set aside. The $7 subscription is easier to budget for than a lump-sum deposit, especially when money is tight.

People Rebuilding After Bankruptcy or Consumer Proposal

After a bankruptcy discharge or completion of a consumer proposal, your credit file is essentially starting over. KOHO Credit Builder provides a no-risk, no-credit-check way to begin adding positive payment history to your Equifax report. Pair it with a secured card once you can afford the deposit, and you have a solid two-product rebuilding strategy.

Students Building Credit for the First Time

If you are a student or young adult with no credit history at all, KOHO offers a gentle introduction to credit building without the responsibility of managing an actual credit card. The app-based budgeting tools can also help you build good financial habits early.

Who Should Skip KOHO Credit Builder?

If you already have multiple active credit accounts in good standing and a score above 680, KOHO Credit Builder is unlikely to move the needle enough to justify $7 per month. You would be better served by focusing on utilization optimization, requesting credit limit increases, or using our calculator to model the impact of specific actions on your score.

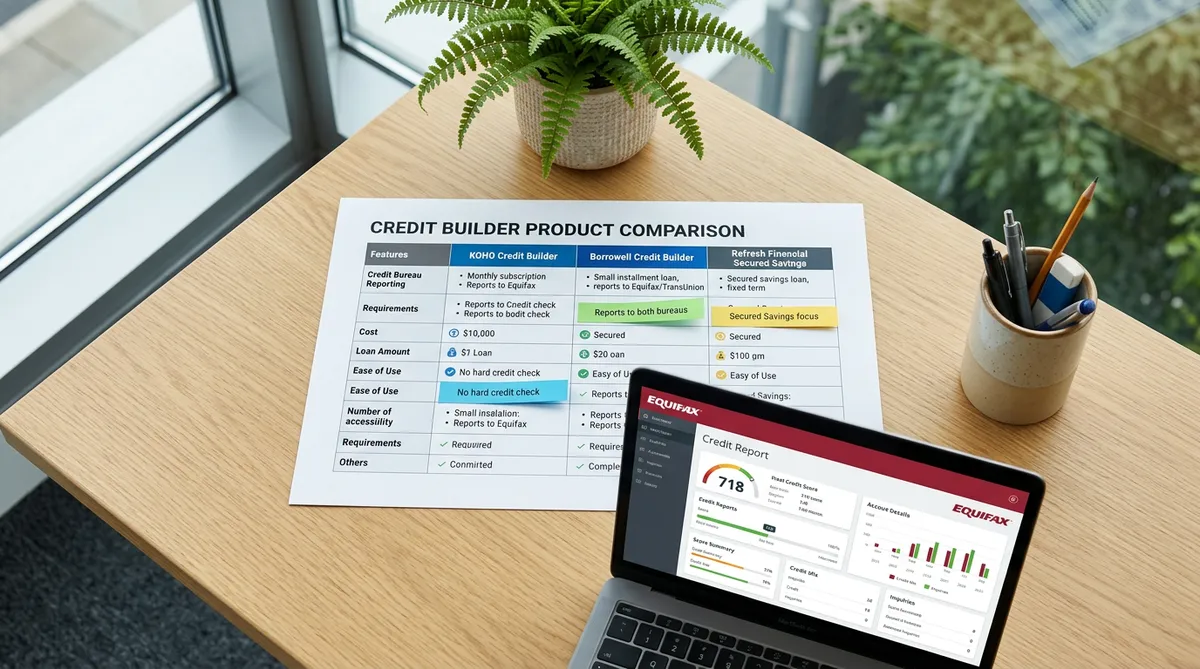

KOHO vs Borrowell Credit Builder vs Refresh Financial

Choosing a credit builder product in Canada comes down to your specific needs, budget, and how quickly you want results. Here is how the three most popular options compare:

KOHO Credit Builder

- Monthly cost: $7 to $15 depending on plan

- How it works: Sets aside your own funds; reports as installment loan to Equifax

- Credit check required: No

- Bureau reporting: Equifax only

- Additional benefits: Prepaid Mastercard, cash back, spending account, budgeting tools

- Best for: People who want an all-in-one financial tool with credit building included

Borrowell Credit Builder

Borrowell offers its own credit builder product that works similarly to KOHO. You make a fixed monthly payment, Borrowell holds the funds, and the activity is reported to Equifax. Borrowell also provides free credit score monitoring (Equifax), which is useful for tracking your progress. The key difference is that Borrowell focuses more narrowly on credit building and monitoring, while KOHO is a broader financial platform.

- Monthly cost: Varies by plan

- How it works: Fixed monthly payments reported as installment activity

- Credit check required: Soft check only

- Bureau reporting: Equifax

- Additional benefits: Free credit score monitoring, personalized product recommendations

- Best for: People who want credit building combined with ongoing score monitoring

Refresh Financial

Refresh Financial takes a different approach. It offers a secured savings loan where you make fixed monthly payments over a set term (typically 12 to 36 months), and the funds accumulate in a locked savings account. At the end of the term, you receive the savings minus fees and interest. Refresh reports to both Equifax and TransUnion, which is a meaningful advantage.

- Monthly cost: Fixed payment amount over the loan term (varies by loan size)

- How it works: Secured savings loan with fixed monthly payments

- Credit check required: Soft check

- Bureau reporting: Equifax and TransUnion

- Additional benefits: Forced savings component; you get a lump sum at the end

- Best for: People who want dual-bureau reporting and a built-in savings mechanism

The Verdict on Comparisons

If dual-bureau reporting is your top priority, Refresh Financial has the edge. If you want a free monitoring tool alongside credit building, Borrowell is a strong choice. If you want the most flexible everyday financial tool that happens to include credit building, KOHO wins. Many people in serious credit-building mode use two of these products simultaneously to maximize tradelines and bureau coverage.

How to Maximize Your Results with KOHO Credit Builder

Simply subscribing to KOHO Credit Builder and forgetting about it will produce results, but you can accelerate your progress with a few intentional moves.

Pair It with a Secured Credit Card

As mentioned above, KOHO only reports to Equifax. Adding a secured credit card like the Capital One Secured Mastercard gives you a revolving tradeline that reports to both Equifax and TransUnion. This combination covers both bureau reporting and both major tradeline types (installment and revolving), which strengthens your credit mix.

Keep Your KOHO Account Funded

KOHO cannot report on-time payments if there is not enough money in your account to cover the Credit Builder amount. Treat your monthly Credit Builder contribution the same way you treat a bill. Set up direct deposit or a recurring transfer so your balance is always sufficient on the reporting date.

Use the KOHO Card for Everyday Spending

The more you use KOHO as your primary spending account, the more cash back you earn, which helps offset the subscription fee. While everyday spending itself does not affect your credit score (since it is a prepaid card, not a credit card), the cash back makes the overall cost of the product lower.

Monitor Your Equifax Report Monthly

Track your score regularly through Borrowell or by requesting your free Equifax report. Watch for the KOHO tradeline to appear (it can take one to two billing cycles), and verify that each month shows as paid on time. If you spot errors, dispute them with Equifax immediately.

Stay Consistent for at Least 12 Months

Credit building is a long game. While you may see early movement in your score within three to six months, the most significant gains come from 12 or more months of uninterrupted on-time payment history. Resist the urge to cancel after two months because you do not see a dramatic jump. Consistency is the most important factor.

Check Your Full Credit Picture

Your KOHO Credit Builder activity is only one piece of the puzzle. Use our calculator to understand how different actions (lowering utilization, adding tradelines, disputing errors) would affect your overall score. A holistic approach always outperforms any single product.

Frequently Asked Questions

Does KOHO Credit Builder do a hard credit check?

No. Signing up for KOHO and activating Credit Builder does not result in a hard inquiry on your credit report. This makes it accessible to people with low scores or no credit history at all. Your score will not take a hit from signing up.

How long does it take to see results from KOHO Credit Builder?

Most users begin to see changes to their Equifax credit report within one to two months of activation, as that is when the tradeline first appears. Meaningful score improvement typically takes three to six months of consistent on-time reporting. Users starting with a thin or empty credit file often see faster initial gains than those with existing negative items.

Can I use KOHO Credit Builder if I have bad credit?

Yes. There is no minimum credit score required to sign up for KOHO or to activate Credit Builder. The product is specifically designed for people who are building or rebuilding credit. Whether your score is in the 400s after a financial setback or you simply have no score at all, you can use KOHO Credit Builder.

Does KOHO report to TransUnion?

No. As of 2026, KOHO Credit Builder reports exclusively to Equifax Canada. It does not report to TransUnion Canada. If you want to build credit on both bureaus simultaneously, you will need to pair KOHO with a product that reports to TransUnion, such as a secured credit card from a major issuer.

Is KOHO Credit Builder better than a secured credit card?

They serve different purposes and are most effective when used together. KOHO Credit Builder creates an installment tradeline on your Equifax report with zero risk of debt accumulation. A secured credit card creates a revolving tradeline (often on both bureaus) and helps build your utilization history. For the strongest credit profile, consider using both. If you can only choose one and have the deposit available, a secured credit card typically delivers broader credit-building benefits because it reports to both bureaus and contributes to your revolving credit history.

Final Verdict: Is KOHO Credit Builder Worth It?

KOHO Credit Builder earns a solid recommendation for a specific audience: Canadians who need a low-cost, low-risk entry point into credit building. If you are a newcomer, a student, someone rebuilding after financial hardship, or anyone who cannot afford a secured card deposit right now, KOHO at $7 per month is a practical and effective tool.

It is not perfect. The lack of TransUnion reporting is a real limitation, and the monthly fee, while modest, does exceed what you would pay for a secured card over time. It also does not replace the credit-building power of a revolving tradeline.

The smartest approach for most Canadians is to use KOHO Credit Builder as one component of a broader strategy. Pair it with a Capital One Secured Mastercard for dual-bureau coverage, monitor your progress through Borrowell, and stay consistent for at least 12 months. Not sure which combination of tools is right for your situation? Take our recovery quiz for a personalized recommendation based on your current credit profile and goals.

Credit building is not glamorous, and no single product will transform your score overnight. But $7 per month and a few minutes of setup can put you on a path toward better financial options, lower interest rates, and the peace of mind that comes with knowing your credit is heading in the right direction.

Get Your Personalized Recovery Plan

Answer 6 quick questions and get a step-by-step plan tailored to your situation.

Take the Free Quiz

Product manager in fintech, immigrant to Canada, and founder of Credit Score Hero. I moved from Kyrgyzstan to Montreal in 2022 and built this site to help Canadians navigate the credit system with free tools and honest, Canada-specific advice.