Does Cancelling a Credit Card Hurt Your Score in Canada?

Closing a credit card in Canada can drop your score 20-50 points. Here's exactly why it happens, when it's worth doing anyway, and how to minimize the damage.

Product Manager in Fintech · Montreal, Canada

Ready to start recovering? Our free quiz creates a personalized plan for your exact situation.

Take the Free Quiz →I closed my CIBC credit card in 2023 — on purpose, after opening the Costco Mastercard CIBC to replace it. Seemed logical. Same bank, better rewards, no reason to keep two cards open.

My Credit Karma score dropped 31 points within 60 days.

No missed payments, no new debt. Just a closed account and a score that suddenly needed explaining. That experience pushed me to actually understand how Equifax Canada calculates scores — and what I learned changed how I think about every card in my wallet.

Does Cancelling a Credit Card Actually Lower Your Score in Canada?

Yes — closing a credit card almost always causes a short-term score drop in Canada. The size of the hit depends on two things: how much of your total available credit that card represents, and how old the account is. For most people, closing one card triggers a 20-40 point drop. Closing your oldest card or your highest-limit card can push that to 50-60 points temporarily.

The good news: it’s usually temporary. Most people recover within 6-12 months, assuming nothing else changes. But if you’re applying for a mortgage or a car loan in the next year, even a 30-point dip can cost you real money in interest rates.

Why Closing a Card Spikes Your Credit Utilization

This is the main mechanism — and most people don’t think it through before they cancel.

Your credit utilization ratio is the percentage of your available credit you’re actually using. Equifax Canada and TransUnion Canada both weight this heavily (roughly 30% of your score). The lower the ratio, the better.

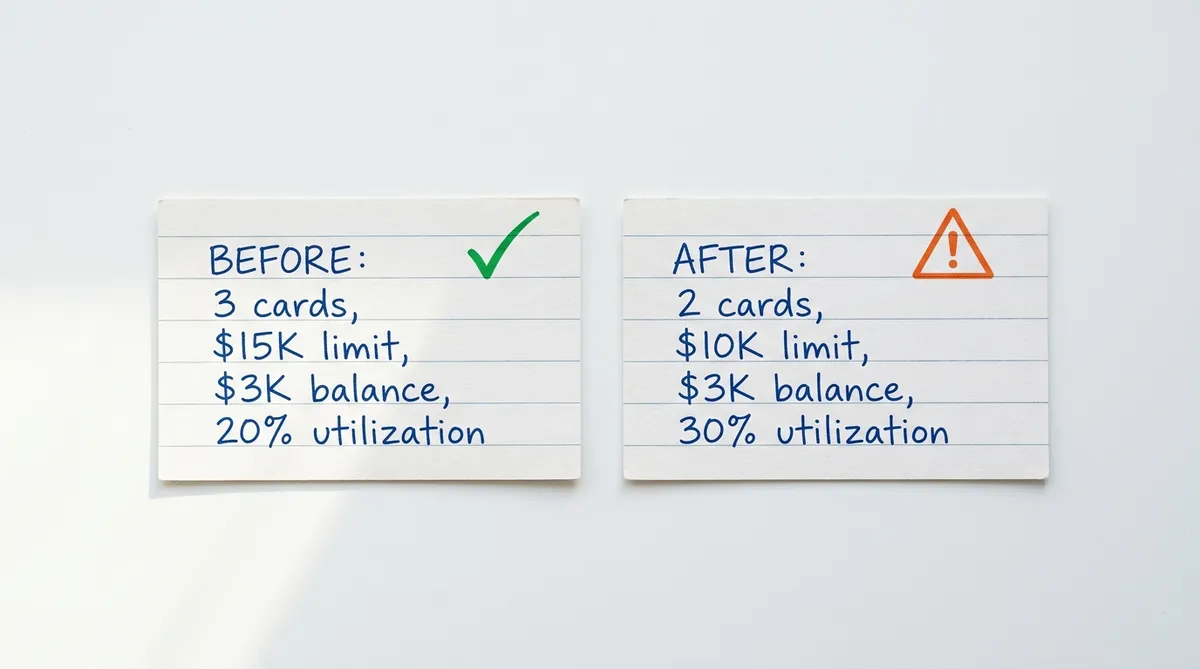

Here’s how the math works:

- You have 3 credit cards with a combined limit of $15,000

- Your current balance across all cards is $3,000

- Your utilization = 20% — solid

Now you cancel one card with a $5,000 limit and a zero balance:

- Combined limit drops to $10,000

- Same $3,000 balance

- Utilization jumps to 30% — worse

You didn’t spend a dollar more. But your score reads it as if you became more financially stretched. That’s the trap.

For a deeper look at how utilization actually works in Canada, read Credit Utilization Ratio in Canada: The 30% Rule Is Wrong — the short version is that 30% isn’t really the threshold you should aim for.

Does Your Credit History Length Take a Hit Too?

Yes, but it’s more complicated than most guides explain.

When you close a card, Equifax Canada doesn’t immediately erase the history. The account stays on your credit report for 6-10 years after closure — closed in good standing stays positive, closed with missed payments stays negative. So your average account age doesn’t collapse overnight.

The real damage comes later. As older accounts eventually age off your report, the average drops. If you’re closing your oldest card today, you’re starting a countdown. In 6-8 years, your average account age could look significantly shorter than it does now — right when you might be applying for a mortgage renewal or a second property.

This matters most if:

- The card you’re cancelling is your oldest account (anything 5+ years)

- You’re planning to apply for a mortgage within the next 2-3 years

If you want to understand how your score affects mortgage eligibility, Credit Score Needed for a Mortgage in Canada (2026) breaks down exactly what lenders want to see.

When Is Cancelling a Card Worth It in Canada?

The honest answer: less often than you think, but sometimes the math still works out.

Good reasons to cancel:

The annual fee isn’t worth it. If you’re paying $120/year for a card you rarely use and the rewards don’t offset the fee, cancelling makes financial sense. A temporary 30-point drop costs less than years of fees.

You upgraded from a secured card. If you moved from a Capital One Guaranteed Secured Mastercard ($59 annual fee, $75 minimum deposit) to an unsecured card, keeping the secured card open has diminishing value. Closing it is defensible.

You have too many cards and it’s getting unmanageable. More cards means more payment due dates, which means a higher chance of missing one. A single missed payment does far more damage than closing an account cleanly.

Bad reasons to cancel:

You’re frustrated with the card. Put a $10 Netflix subscription on it, set up autopay, and forget it exists. That’s cheaper than closing it.

You think fewer cards signals better financial discipline. It doesn’t — not in Canada. Equifax Canada doesn’t penalize you for having multiple cards in good standing. Length of relationship and diversity of credit types both help.

Someone told you American advice applies here. It usually doesn’t. Chapter 7 bankruptcy, FICO scores, credit unions behaving like banks — a lot of what you read online is written for the US market. Canadian credit scoring works differently.

What Happens to Your Credit Mix When You Cancel?

Credit mix — having different types of credit — accounts for roughly 10% of your Equifax Canada score. Credit cards, auto loans, mortgages, lines of credit. Not the biggest factor, but it compounds with everything else.

As of April 2026, I have a mortgage, a car lease, one credit card (Costco Mastercard CIBC), and a credit line at Scotiabank. That mix tells Equifax I can handle different types of debt responsibly. If I closed the credit card and only had the mortgage and lease, the mix narrows — slightly weaker signal across the board.

If cancelling a card would leave you with only one remaining credit account, that’s worth pausing over. You’re not just losing the available limit, you’re losing diversity.

How to Cancel a Card Without Trashing Your Score

If you’ve decided cancelling is the right call, here’s how to reduce the damage:

Pay down your other balances first. Before closing the card, get your utilization on remaining cards below 10%. That creates a buffer — when the cancelled card’s limit disappears, your overall utilization doesn’t spike as hard.

Request a credit limit increase on a card you’re keeping. Banks are often willing to increase limits for reliable customers. A $2,000-$3,000 increase on another card partially offsets the lost limit from the cancelled one.

Don’t cancel before a major credit application. If you’re applying for a mortgage in the next 6 months, just wait. The temporary dip from cancellation, combined with the hard inquiry from a mortgage application, can push you into a worse rate bracket.

Redeem any points before you call. This sounds obvious but people forget. Confirm your points balance is zero before the account closes — points disappear when the account does.

Get written confirmation. Ask for an email or letter confirming the account was closed at your request and in good standing. This matters if there’s ever a dispute on your Equifax or TransUnion report later.

What I Wish I’d Known Before Closing That First Card

When I switched from my CIBC credit card to the Costco Mastercard, I assumed closing the old one was routine housekeeping. Same bank, clean transition, no reason to keep a card with weaker rewards.

What I missed: that original CIBC card was my second-oldest credit account in Canada. Opening a new card doesn’t replace the history of an old one. The Costco card had zero history on the day I opened it. The CIBC card I closed had 18 months of clean payment history — not long, but real. And because the Costco card started with a lower limit than what I’d just closed, my utilization went up at the same time.

I caught the score drop through Credit Karma Canada, which I use for ongoing monitoring. Honestly, Credit Karma does more than just show your number. At one point it flagged a mobile plan someone had signed up in my name — framed as “free” but actually carrying a monthly fee that was being reported to the credit bureaus. I caught it early and disputed it before it did any real damage. If you’re not monitoring, How to Get a Free Credit Score in Canada (No Tricks, No Trials) covers both Borrowell and Credit Karma Canada — both are genuinely free, no trial nonsense.

My score is 820 as of April 2026. The 31-point drop from closing the CIBC card recovered in about 8 months. But I wasn’t buying a house or car during that window. If I’d cancelled during a mortgage application process, I’d have been looking at a higher interest rate — and on a Canadian mortgage, even 0.1% higher over 5 years is real money.

The Short Answer

Cancelling a credit card in Canada will usually drop your score by 20-50 points. The hit is temporary — typically 6-12 months — but it’s real. The main cause is a jump in your credit utilization ratio, not the loss of history (that comes later, gradually).

Don’t cancel unless the annual fee genuinely isn’t worth it, or you’re consolidating for a real reason. If you do cancel, pay down other balances first, try to get a limit increase somewhere else, and don’t do it within 6 months of a major credit application.

Not sure where your score stands right now — or what’s actually dragging it down? Take the 90-second credit recovery quiz for a clear picture of your current situation and what’s actually moving your number.

Related: Credit Utilization Ratio in Canada: The 30% Rule Is Wrong (Here’s Why) · Best Secured Credit Cards for Bad Credit in Canada 2026

Get Your Personalized Recovery Plan

Answer 6 quick questions and get a step-by-step plan tailored to your situation.

Take the Free Quiz

Product manager in fintech, immigrant to Canada, and founder of Credit Score Hero. I moved from Kyrgyzstan to Montreal in 2022 and built this site to help Canadians navigate the credit system with free tools and honest, Canada-specific advice.